Anti-VEGF Therapeutics Market

Anti-VEGF Therapeutics Market

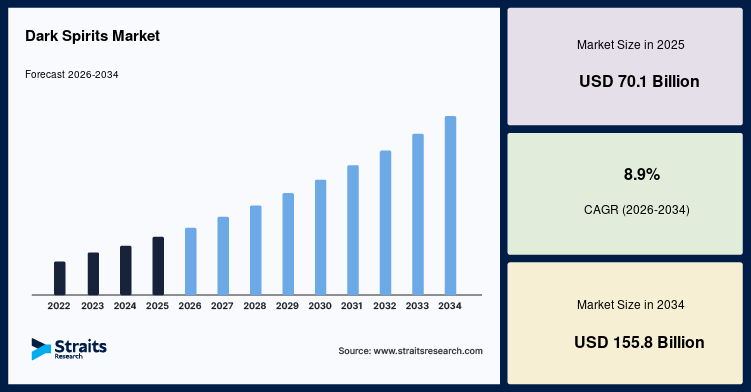

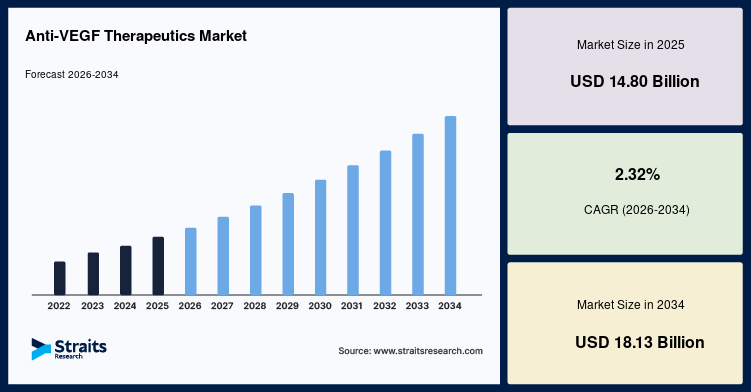

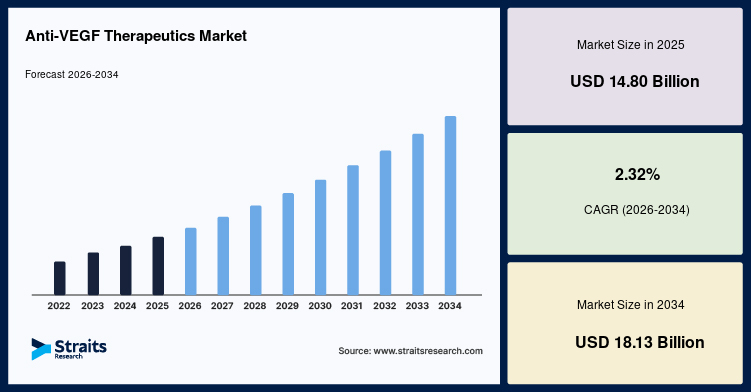

The Anti-VEGF Therapeutics Market is witnessing steady growth as the prevalence of retinal disorders and chronic ophthalmic diseases continues to rise worldwide. The market size was valued at USD 14.80 billion in 2025 and is projected to grow from USD 15.09 billion in 2026 to USD 18.13 billion by 2034, registering a CAGR of 2.32% during the forecast period (2026–2034). Growing awareness regarding early diagnosis, continuous advancements in biologic therapies, and increasing adoption of innovative anti-VEGF drugs are expected to support market expansion throughout the forecast period.

The increasing burden of age-related macular degeneration (AMD), diabetic retinopathy, retinal vein occlusion, and diabetic macular edema has significantly increased the demand for anti-VEGF therapeutics. Pharmaceutical companies are investing in next-generation biologics, extended-duration formulations, and dual-pathway therapies to improve patient outcomes while reducing treatment frequency, creating favorable growth opportunities across global healthcare markets.

For detailed market insights, growth forecasts, and competitive analysis, visit: https://straitsresearch.com/report/anti-vegf-therapeutics-market

Market Drivers

Rising Prevalence of Retinal Disorders

The growing incidence of retinal diseases remains one of the strongest drivers for the Anti-VEGF Therapeutics Market. An aging global population has contributed to a higher prevalence of age-related macular degeneration, while increasing diabetes cases continue to drive diabetic retinopathy and diabetic macular edema worldwide. Since anti-VEGF therapy remains the standard treatment for many of these vision-threatening conditions, healthcare providers continue to adopt these therapies at a steady pace.

Technological Advancements in Anti-VEGF Therapies

Continuous innovation in biologic drug development is transforming the treatment landscape. Manufacturers are introducing higher-concentration formulations, bispecific antibodies, and therapies capable of extending dosing intervals. These advancements reduce the burden of frequent intravitreal injections while improving patient compliance, physician confidence, and long-term clinical outcomes. Extended-release drug delivery systems and refillable ocular implants are also reshaping therapeutic approaches.

Growing Investment in Ophthalmology Research

Pharmaceutical companies are significantly increasing investments in ophthalmology research and development. Clinical trials focusing on dual-target mechanisms, biosimilars, sustained-release delivery technologies, and gene-based approaches are expanding the therapeutic pipeline. These innovations are expected to improve efficacy while providing more personalized treatment options for patients suffering from retinal vascular diseases.

Expanding Healthcare Infrastructure

Emerging economies continue to strengthen healthcare infrastructure through investments in specialized ophthalmology centers, retinal screening programs, and advanced diagnostic technologies. Government initiatives promoting early diagnosis and vision preservation have further improved patient access to anti-VEGF therapies, particularly across Asia-Pacific and Latin America.

Market Challenges

High Treatment Costs

Despite their clinical effectiveness, anti-VEGF therapeutics remain expensive for many patients, particularly in countries with limited reimbursement coverage. The requirement for repeated injections over several years can significantly increase overall treatment costs, limiting accessibility in lower-income healthcare systems.

Frequent Treatment Requirements

Most currently approved anti-VEGF therapies require regular intravitreal injections to maintain vision outcomes. Frequent hospital visits may reduce patient adherence, particularly among elderly individuals with mobility limitations. Although newer long-acting therapies are addressing this challenge, treatment burden remains an important market restraint.

Biosimilar Competition

The expiration of patents for several leading anti-VEGF products has accelerated biosimilar development. While biosimilars improve affordability and patient access, they also intensify pricing pressure for branded manufacturers. Companies must therefore continue investing in differentiated products, novel delivery systems, and improved clinical efficacy to maintain competitive advantages.

Market Segmentation

By Product

The Anti-VEGF Therapeutics Market is segmented into Eylea, Lucentis, Beovu, Vabysmo, and Others.

Eylea dominated the global market in 2025 owing to its proven clinical efficacy, broad regulatory approvals, and extended dosing intervals that reduce treatment frequency. Its strong physician acceptance and effectiveness across multiple retinal diseases have helped maintain market leadership.

Meanwhile, Vabysmo is anticipated to witness the fastest growth during the forecast period. Its dual mechanism targeting both VEGF and Ang-2 pathways offers improved durability and enhanced disease control, making it an attractive option for long-term retinal disease management.

By Disease Type

Based on disease type, the market is segmented into:

-

Macular Edema

-

Diabetic Retinopathy

-

Retinal Vein Occlusion

-

Age-related Macular Degeneration

-

Myopic Choroidal Neovascularization

Among these, Age-related Macular Degeneration (AMD) accounted for the largest market share in 2025 due to its high prevalence among the elderly population and its position as one of the leading causes of irreversible vision loss globally. Increasing life expectancy continues to support long-term demand for anti-VEGF therapies.

The Macular Edema segment is projected to experience strong growth throughout the forecast period, supported by increasing diabetes prevalence, improved diagnostic capabilities, and greater awareness regarding early intervention.

By Distribution Channel

The Anti-VEGF Therapeutics Market is further segmented by distribution channel into hospital pharmacies, specialty pharmacies, retail pharmacies, and online pharmacies.

Hospital pharmacies account for the largest market share due to the specialized administration of anti-VEGF therapies. Since these drugs are typically delivered through intravitreal injections performed by ophthalmologists and retina specialists, hospitals and specialty eye care centers remain the primary distribution channels. Their access to advanced diagnostic equipment and skilled healthcare professionals further strengthens this segment’s dominance.

Specialty pharmacies are also experiencing notable growth as they support the distribution of high-value biologics, streamline reimbursement processes, and provide patient assistance services. Meanwhile, retail and online pharmacies are gradually expanding their presence in markets where regulations permit the dispensing of specialty pharmaceutical products.

By Region

The global Anti-VEGF Therapeutics Market is geographically segmented into North America, Europe, Asia-Pacific, and Latin America, Middle East & Africa. Market performance varies across these regions based on healthcare infrastructure, reimbursement policies, disease prevalence, regulatory approvals, and access to advanced ophthalmic care.

Regional Insights

North America

North America continues to dominate the Anti-VEGF Therapeutics Market due to its advanced healthcare infrastructure, high healthcare expenditure, and widespread adoption of innovative biologic therapies. The United States accounts for the largest regional share, supported by the high prevalence of age-related macular degeneration, diabetic retinopathy, and retinal vein occlusion. Favorable reimbursement policies, extensive clinical research, and the strong presence of leading pharmaceutical companies further contribute to regional market growth. Continuous product approvals and investments in ophthalmology research are expected to sustain North America’s leadership throughout the forecast period.

Europe

Europe represents a significant share of the global market, driven by an aging population, increasing awareness of retinal diseases, and well-established healthcare systems. Countries including Germany, the United Kingdom, France, Italy, and Spain continue to witness strong demand for anti-VEGF therapies due to improved screening programs and access to specialized ophthalmic care. Regulatory support for biosimilars is also helping expand treatment accessibility while encouraging competition among manufacturers.

Asia-Pacific

Asia-Pacific is expected to register the fastest growth during the forecast period. Rapidly aging populations, rising diabetes prevalence, expanding healthcare infrastructure, and improving access to advanced ophthalmic treatments are driving market expansion across China, Japan, India, South Korea, and Southeast Asian countries. Governments are increasingly investing in retinal disease awareness campaigns and healthcare modernization, while pharmaceutical companies continue expanding their commercial presence across the region. Rising disposable incomes and greater availability of innovative therapies are expected to create substantial long-term growth opportunities.

Latin America, Middle East & Africa

The Latin America, Middle East & Africa region presents emerging opportunities for market participants. Improving healthcare infrastructure, increasing diagnosis rates, and expanding access to specialty ophthalmic care are contributing to market development in several countries. Although reimbursement limitations and unequal access to healthcare remain challenges in certain markets, ongoing government healthcare initiatives and private-sector investments are gradually improving patient access to anti-VEGF therapies.

Key Players Analysis

The Anti-VEGF Therapeutics Market is highly competitive, with leading pharmaceutical companies focusing on biologic innovation, next-generation retinal therapies, biosimilar development, and strategic collaborations. Companies continue to invest heavily in clinical research to improve treatment durability, reduce injection frequency, and enhance patient outcomes. The competitive landscape is also shaped by regulatory approvals, acquisitions, licensing agreements, and expansion into emerging healthcare markets.

Key companies operating in the market include:

-

Regeneron Pharmaceuticals, Inc.

-

F. Hoffmann-La Roche Ltd.

-

Genentech, Inc.

-

Novartis AG

-

Bayer AG

-

Biogen Inc.

-

Samsung Bioepis Co., Ltd.

-

Biocon Biologics Ltd.

-

Amgen Inc.

-

Outlook Therapeutics, Inc.

-

Kodiak Sciences Inc.

-

Adverum Biotechnologies, Inc.

-

Chengdu Kanghong Pharmaceutical Group Co., Ltd.

-

Coherus BioSciences, Inc.

-

Formycon AG

Conclusion

The Anti-VEGF Therapeutics Market is expected to maintain steady growth through 2034, driven by the increasing prevalence of retinal diseases, continuous innovation in biologic therapies, and expanding access to specialized ophthalmic care worldwide. Advances in long-acting formulations, dual-target therapies, and biosimilar products are improving treatment effectiveness while enhancing patient convenience and affordability. Although challenges such as high treatment costs and reimbursement limitations persist, ongoing investments in research and healthcare infrastructure are expected to create sustainable growth opportunities. As the market is projected to reach USD 18.13 billion by 2034, companies that prioritize innovation, strategic partnerships, and patient-centered treatment solutions will be well-positioned to strengthen their market presence.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)