Point-of-Care Coagulation Testing Devices Market

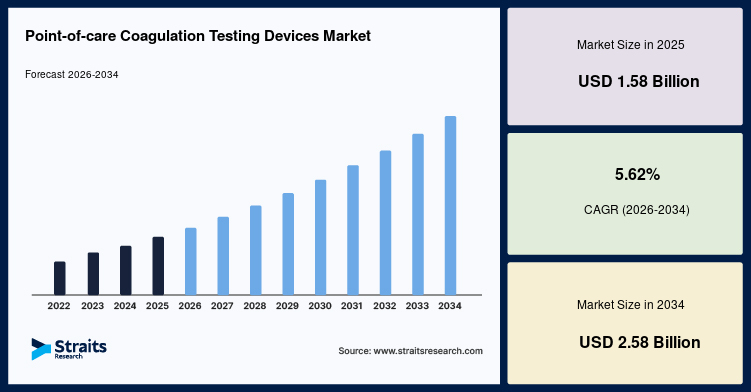

The global point-of-care coagulation testing devices market is witnessing steady growth due to the increasing prevalence of cardiovascular disorders, rising demand for rapid diagnostic solutions, and expanding adoption of decentralized healthcare. The point-of-care coagulation testing devices market size was valued at USD 1.58 billion in 2025 and is projected to grow from USD 1.66 billion in 2026 to USD 2.58 billion by 2034 at a CAGR of 5.62% during the forecast period (2026–2034). North America accounted for the largest point-of-care coagulation testing devices market share of 41.30% in 2025.

Point-of-care coagulation testing devices enable healthcare professionals to rapidly measure blood clotting parameters directly at the patient’s bedside, in clinics, emergency departments, or even at home. These devices help clinicians make timely treatment decisions, particularly for patients receiving anticoagulant therapy or undergoing surgery. Growing emphasis on faster diagnostics, personalized patient care, and improved clinical outcomes continues to support market expansion.

For detailed market insights, growth forecasts, and competitive analysis, visit:

https://straitsresearch.com/report/point-of-care-coagulation-testing-devices-market

Market Drivers

Rising Prevalence of Cardiovascular Diseases

The growing incidence of cardiovascular disorders, stroke, atrial fibrillation, and venous thromboembolism has significantly increased the need for coagulation monitoring. Patients receiving anticoagulant therapy require frequent blood clotting assessments, making point-of-care devices an essential component of modern healthcare.

The increasing aging population further contributes to rising demand for rapid coagulation testing solutions.

Growing Adoption of Point-of-Care Diagnostics

Healthcare providers are increasingly shifting toward decentralized diagnostic services that provide faster clinical results and improve patient management. Point-of-care coagulation testing devices deliver immediate results, reducing laboratory turnaround times and enabling quicker treatment decisions.

The expansion of outpatient care and home healthcare services is further accelerating market growth.

Technological Advancements in Diagnostic Devices

Manufacturers continue developing compact, user-friendly, and highly accurate coagulation analyzers with wireless connectivity, digital data management, and automated calibration features. These innovations improve workflow efficiency while reducing the risk of testing errors.

Integration with electronic health records and cloud-based healthcare platforms is further enhancing device capabilities.

Market Challenges

High Cost of Advanced Testing Devices

Advanced point-of-care coagulation analyzers and testing consumables may represent a significant investment for smaller healthcare facilities and clinics. Cost considerations may limit adoption in resource-constrained healthcare systems.

Manufacturers continue working to improve affordability while maintaining testing accuracy.

Regulatory Compliance Requirements

Medical diagnostic devices must comply with stringent regulatory standards regarding accuracy, safety, and quality assurance. Achieving regulatory approvals can increase development costs and product launch timelines.

Continuous quality improvement remains essential for maintaining market competitiveness.

Market Segmentation

By Product Type

The market is segmented into coagulation analyzers, test strips, cartridges, reagents, and accessories. Coagulation analyzers account for a significant market share due to their widespread use in hospitals, emergency departments, and outpatient clinics.

Consumables continue generating recurring revenue as testing volumes increase globally.

By Test Type

The market includes prothrombin time (PT), international normalized ratio (INR), activated clotting time (ACT), activated partial thromboplastin time (aPTT), and other coagulation tests. PT/INR testing dominates the market because of its critical role in monitoring patients receiving anticoagulant therapy.

ACT testing is also widely adopted during cardiovascular surgeries and interventional procedures.

By End User

Hospitals, diagnostic laboratories, ambulatory surgical centers, physician offices, and home healthcare settings represent the major end users. Hospitals remain the largest end-user segment due to high patient volumes and increasing emergency care requirements.

Home healthcare is expected to witness strong growth as remote patient monitoring becomes more common.

Regional Insights

North America

North America dominated the point-of-care coagulation testing devices market with a 41.30% share in 2025. The region benefits from advanced healthcare infrastructure, widespread adoption of rapid diagnostic technologies, favorable reimbursement policies, and increasing prevalence of cardiovascular diseases.

Europe

Europe represents a significant market supported by growing demand for decentralized diagnostics, increasing healthcare investments, and expanding elderly populations. Germany, the United Kingdom, France, and Italy remain major regional contributors.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth during the forecast period. Rising healthcare expenditure, increasing awareness of early disease diagnosis, expanding hospital infrastructure, and growing chronic disease burden are driving market expansion across China, India, Japan, and South Korea.

Government initiatives to improve healthcare accessibility further support regional growth.

Latin America, Middle East & Africa

These regions are gradually adopting point-of-care diagnostic technologies as healthcare infrastructure improves and access to modern diagnostic equipment expands. Increasing investments in healthcare modernization are expected to create new growth opportunities.

Key Players Analysis

The point-of-care coagulation testing devices market is highly competitive, with manufacturers focusing on portable diagnostic systems, digital connectivity, enhanced testing accuracy, and user-friendly interfaces. Companies continue investing in product innovation, strategic partnerships, and global distribution networks to strengthen their market presence.

Advancements in wireless monitoring, cloud-based data management, and miniaturized diagnostic technologies are expected to shape the future of the industry.

Key Companies

-

Roche Diagnostics

-

Siemens Healthineers AG

-

Abbott Laboratories

-

Werfen

-

Sysmex Corporation

-

Danaher Corporation

-

Thermo Fisher Scientific Inc.

-

HORIBA, Ltd.

-

SEKISUI Diagnostics

-

Trivitron Healthcare

Conclusion

The global point-of-care coagulation testing devices market is expected to experience steady growth through 2034, driven by rising cardiovascular disease prevalence, increasing demand for rapid diagnostics, and continuous technological advancements in point-of-care testing. While device costs and regulatory challenges remain important considerations, expanding home healthcare, decentralized diagnostics, and digital healthcare integration are expected to create significant growth opportunities. As healthcare systems continue prioritizing faster and more efficient patient care, point-of-care coagulation testing devices will remain a vital component of modern diagnostic services.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)