Fuel Cell Market Forecast, 2034

The global fuel cell market is witnessing remarkable growth, driven by increasing demand for clean energy solutions, rising investments in hydrogen infrastructure, and growing adoption of fuel cell technology across transportation, stationary power generation, and portable power applications. According to the latest report by Straits Research, the global fuel cell market is expected to register significant growth during the forecast period 2026–2034. Government initiatives supporting decarbonization, expanding hydrogen economies, and advancements in fuel cell technologies are key factors driving market expansion.

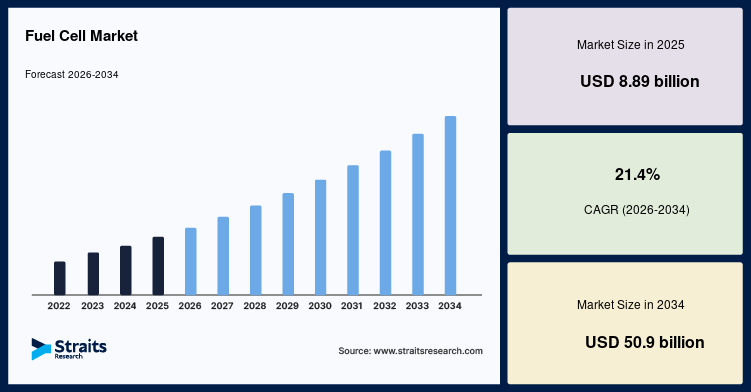

The global fuel cell market size was valued at USD 8.89 billion in 2025 and is projected to grow from USD 10.79 billion in 2026 to USD 50.9 billion by 2034 at a CAGR of 21.4% during the forecast period 2026-2034.

Market Drivers

The primary driver of the fuel cell market is the global transition toward clean and low-carbon energy. Governments and industries are increasingly adopting fuel cell technologies to reduce greenhouse gas emissions and achieve net-zero carbon targets. Fuel cells generate electricity through an electrochemical process with minimal emissions, making them an attractive alternative to conventional fossil fuel-based power generation.

Another significant growth driver is the expanding hydrogen infrastructure. Public and private investments in hydrogen production, storage, transportation, and refueling stations are accelerating the commercialization of fuel cell electric vehicles (FCEVs) and stationary fuel cell systems. The development of green hydrogen projects is further strengthening market growth.

The growing adoption of fuel cell electric vehicles (FCEVs) is also contributing to market expansion. Automotive manufacturers are investing in hydrogen-powered passenger cars, buses, trucks, trains, and marine vessels to provide longer driving ranges, faster refueling, and lower emissions compared to battery-electric alternatives for heavy-duty transportation.

Additionally, increasing demand for reliable backup power and distributed energy generation is creating new opportunities for stationary fuel cell systems. Data centers, hospitals, telecommunication networks, and commercial facilities are deploying fuel cells to ensure uninterrupted power supply and improve energy efficiency.

Market Challenges

Despite favorable growth prospects, the fuel cell market faces several challenges. One of the major concerns is the high production and installation cost of fuel cell systems, particularly proton exchange membrane (PEM) and solid oxide fuel cells, which may limit widespread adoption.

Another challenge is the limited hydrogen refueling infrastructure, especially in developing economies, making large-scale deployment of hydrogen-powered vehicles more difficult.

The market also faces challenges related to hydrogen production and storage. Producing green hydrogen at competitive costs and ensuring safe transportation and storage remain key technical and economic challenges.

Furthermore, competition from battery-electric technologies and evolving renewable energy solutions may affect market penetration in certain applications.

Market Segmentation

The fuel cell market is segmented based on type, application, fuel type, and end user.

By type, the market includes Proton Exchange Membrane Fuel Cells (PEMFC), Solid Oxide Fuel Cells (SOFC), Phosphoric Acid Fuel Cells (PAFC), Molten Carbonate Fuel Cells (MCFC), Alkaline Fuel Cells (AFC), and Direct Methanol Fuel Cells (DMFC). Proton Exchange Membrane Fuel Cells dominate the market due to their high efficiency, compact design, rapid start-up capability, and widespread adoption in transportation and portable power applications.

By application, the market is segmented into transportation, stationary power generation, and portable power. The transportation segment accounts for the largest market share owing to increasing deployment of fuel cell electric vehicles, hydrogen buses, commercial trucks, rail systems, and marine vessels.

By fuel type, the market includes hydrogen, methanol, natural gas, biogas, and others. Hydrogen dominates the market due to its high energy density, clean emissions profile, and growing availability through green hydrogen initiatives.

By end user, the market comprises automotive, utilities, industrial, residential, commercial, aerospace & defense, and others. The automotive sector remains the largest end-user segment due to increasing investments in hydrogen mobility and fuel cell-powered transportation solutions.

Regional Insights

Regionally, the fuel cell market is analyzed across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Asia-Pacific dominates the global fuel cell market due to strong government support, expanding hydrogen infrastructure, and increasing adoption of fuel cell technologies across Japan, South Korea, China, and other regional economies. Significant investments in hydrogen-powered transportation and clean energy projects continue to drive market growth.

Europe holds a substantial market share, supported by ambitious decarbonization targets, growing hydrogen economy initiatives, increasing renewable energy integration, and strong investments in fuel cell-powered mobility and industrial applications.

North America represents a significant market owing to increasing deployment of stationary fuel cells, expanding hydrogen production projects, government funding for clean energy technologies, and growing investments in fuel cell vehicles.

Latin America is gradually emerging as a promising market with increasing renewable energy investments, industrial decarbonization initiatives, and growing interest in hydrogen-based energy systems.

The Middle East & Africa is expected to witness steady growth due to rising investments in green hydrogen production, clean energy infrastructure, and large-scale renewable energy projects.

Key Players Analysis

The fuel cell market is highly competitive, with leading companies focusing on hydrogen technologies, fuel cell efficiency improvements, production capacity expansion, and strategic collaborations.

Key companies operating in the market include Ballard Power Systems Inc., Plug Power Inc., Bloom Energy Corporation, FuelCell Energy, Inc., Doosan Fuel Cell Co., Ltd., Cummins Inc., Panasonic Holdings Corporation, Toshiba Energy Systems & Solutions Corporation, Ceres Power Holdings plc, and SFC Energy AG.

These companies are investing significantly in research and development to improve fuel cell durability, reduce production costs, expand hydrogen infrastructure partnerships, and commercialize next-generation fuel cell technologies. Strategic acquisitions, joint ventures, and government-supported projects continue to strengthen their competitive position in the global fuel cell market.

For detailed insights, visit: https://straitsresearch.com/report/fuel-cell-market

About Us

Straits Research is a leading research and intelligence organization, specializing in research, analytics, and advisory services, along with providing business insights and research reports.

Contact Us

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.)