Next-Generation Cancer Diagnostics Market

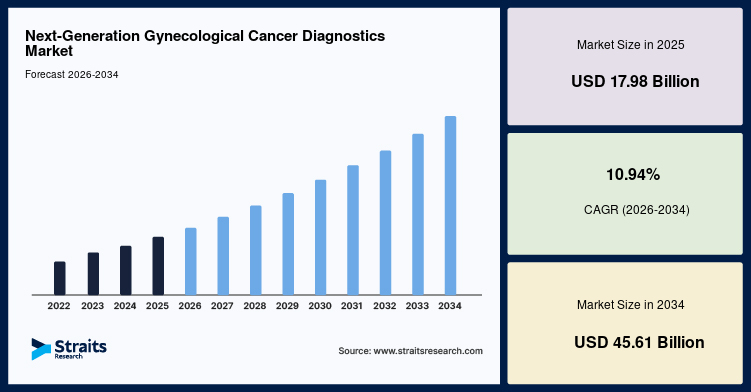

The global next-generation cancer diagnostics market is witnessing rapid growth due to increasing cancer prevalence, rising adoption of precision medicine, and continuous advancements in molecular diagnostic technologies. The global next-generation cancer diagnostics market size is estimated at USD 17.98 billion in 2025 and is projected to reach USD 45.61 billion by 2034, growing at a CAGR of 10.94% during the forecast period. Strong market growth is supported by expanding government and private initiatives focused on improving cancer diagnosis, early detection, and patient care.

Next-generation cancer diagnostics combine advanced technologies such as next-generation sequencing (NGS), liquid biopsy, molecular diagnostics, artificial intelligence, and genomic profiling to detect cancer with greater speed and accuracy. These technologies help clinicians identify genetic mutations, personalize treatment strategies, and improve patient outcomes. Increasing investments in oncology research and precision healthcare continue to accelerate the adoption of next-generation diagnostic solutions worldwide.

For detailed market insights, growth forecasts, and competitive analysis, visit:

https://straitsresearch.com/report/next-generation-gynecological-cancer-diagnostics-market

Market Drivers

Growing Government and Private Investments in Cancer Care

Governments and private healthcare organizations are increasing investments in cancer screening programs, diagnostic infrastructure, and oncology research. National cancer control initiatives and funding for early detection programs are encouraging healthcare providers to adopt advanced diagnostic technologies.

These investments continue to improve access to high-quality cancer diagnostics while supporting market growth.

Rising Demand for Precision Medicine

Precision medicine is transforming cancer treatment by enabling therapies tailored to an individual’s genetic profile. Next-generation diagnostics identify specific genetic alterations and biomarkers that guide treatment selection and improve clinical outcomes.

The increasing use of targeted therapies continues to drive demand for advanced molecular testing technologies.

Technological Advancements in Molecular Diagnostics

Rapid innovation in genomic sequencing, liquid biopsy, artificial intelligence, and bioinformatics has significantly improved cancer detection capabilities. These technologies provide faster results, greater diagnostic accuracy, and minimally invasive testing options.

Continuous technological development is expanding the clinical applications of next-generation cancer diagnostics.

Market Challenges

High Cost of Advanced Diagnostic Technologies

Next-generation diagnostic platforms require sophisticated laboratory infrastructure, specialized equipment, and skilled professionals. The high cost of testing and implementation may limit adoption in resource-constrained healthcare systems.

Increasing automation and technological advancements are expected to improve affordability over time.

Regulatory and Validation Requirements

Advanced cancer diagnostic technologies must undergo rigorous clinical validation and regulatory approval before commercialization. Meeting evolving regulatory standards can increase development timelines and operational complexity.

Manufacturers continue investing in clinical research to demonstrate diagnostic accuracy and safety.

Market Segmentation

By Technology

The market is segmented into next-generation sequencing, polymerase chain reaction (PCR), liquid biopsy, immunohistochemistry, fluorescence in situ hybridization (FISH), and other molecular diagnostic technologies. Next-generation sequencing accounts for the largest market share due to its ability to analyze multiple genetic biomarkers simultaneously.

Liquid biopsy is expected to witness the fastest growth owing to its minimally invasive nature and growing clinical adoption.

By Cancer Type

The market serves breast cancer, lung cancer, colorectal cancer, gynecological cancer, prostate cancer, blood cancer, and other oncology applications. Lung and breast cancer diagnostics represent major market segments because of their high disease prevalence and increasing use of molecular testing.

Gynecological cancer diagnostics continue expanding with improvements in genomic profiling technologies.

By End User

Hospitals, diagnostic laboratories, cancer research institutes, and specialty oncology centers represent the primary end users. Hospitals account for the largest market share due to increasing patient volumes and expanding precision oncology programs.

Diagnostic laboratories continue investing in advanced molecular testing platforms to improve testing capacity and turnaround times.

Regional Insights

North America

North America dominates the next-generation cancer diagnostics market due to advanced healthcare infrastructure, strong government funding, widespread adoption of precision medicine, and continuous technological innovation. The United States remains the largest regional market.

Europe

Europe represents a significant market supported by expanding cancer screening programs, growing investments in genomic medicine, and favorable healthcare policies. Germany, the United Kingdom, France, and Italy continue driving regional growth.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth during the forecast period. Rising cancer incidence, expanding healthcare infrastructure, increasing government healthcare spending, and growing investments in biotechnology are driving market expansion across China, India, Japan, and South Korea.

Growing awareness of early cancer detection further strengthens regional demand.

Latin America, Middle East & Africa

These regions are gradually improving access to advanced cancer diagnostics through healthcare modernization and increasing public health investments. Expanding oncology services are expected to create future growth opportunities.

Key Players Analysis

The next-generation cancer diagnostics market is highly competitive, with leading companies focusing on genomic sequencing technologies, molecular diagnostic platforms, artificial intelligence, and companion diagnostics. Companies continue investing in research, product innovation, and strategic collaborations to strengthen their competitive positions and improve diagnostic accuracy.

The integration of digital pathology, AI-powered analytics, and precision oncology solutions is expected to drive future market innovation.

Key Companies

-

Illumina, Inc.

-

Thermo Fisher Scientific Inc.

-

F. Hoffmann-La Roche Ltd.

-

QIAGEN N.V.

-

Agilent Technologies, Inc.

-

Bio-Rad Laboratories, Inc.

-

Guardant Health, Inc.

-

Exact Sciences Corporation

-

BGI Genomics Co., Ltd.

-

Myriad Genetics, Inc.

Conclusion

The global next-generation cancer diagnostics market is expected to experience strong growth through 2034, driven by increasing cancer prevalence, expanding government and private healthcare initiatives, and rapid advancements in molecular diagnostic technologies. Although high testing costs and regulatory challenges remain, continuous innovation in genomic sequencing, liquid biopsy, and precision medicine is expected to create significant opportunities for market participants. As healthcare systems increasingly prioritize early cancer detection and personalized treatment, next-generation cancer diagnostics will remain a cornerstone of modern oncology.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)