Biopharmaceutical Third-party Logistics Market Analysis 2034

The global biopharmaceutical third-party logistics market is witnessing significant growth, driven by increasing demand for biologics and specialty pharmaceuticals, expanding cold chain logistics infrastructure, rising outsourcing of supply chain operations, and growing investments in healthcare and pharmaceutical manufacturing. Biopharmaceutical companies are increasingly partnering with third-party logistics (3PL) providers to enhance supply chain efficiency, ensure regulatory compliance, and reduce operational costs.

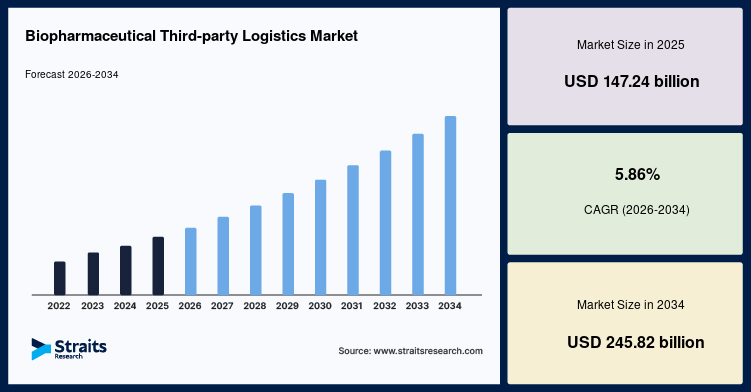

The global biopharmaceutical third-party logistics market size was valued at USD 147.24 billion in 2025 and is projected to grow from USD 155.87 billion in 2026 to USD 245.82 billion by 2034 at a CAGR of 5.86% during the forecast period 2026-2034.

Biopharmaceutical third-party logistics involves outsourced transportation, warehousing, inventory management, cold chain distribution, packaging, and supply chain management services for biologics, vaccines, cell and gene therapies, biosimilars, and other temperature-sensitive pharmaceutical products. The increasing complexity of biologic therapies and the growing need for secure, traceable, and temperature-controlled logistics solutions are expected to drive market growth throughout the forecast period.

Market Drivers

Rising Demand for Biopharmaceutical Products

The growing adoption of biologics, monoclonal antibodies, vaccines, and gene therapies is significantly increasing the need for specialized logistics services capable of maintaining product integrity throughout the supply chain.

Expansion of Cold Chain Logistics

Temperature-sensitive biopharmaceutical products require advanced cold chain transportation and storage solutions. Continuous investments in refrigerated logistics infrastructure are supporting market growth.

Increasing Outsourcing of Supply Chain Operations

Pharmaceutical manufacturers are increasingly outsourcing logistics functions to specialized third-party providers to improve operational efficiency, reduce costs, and focus on core business activities.

Growth of Cell and Gene Therapies

The commercialization of advanced therapies requiring highly controlled transportation conditions is creating substantial demand for specialized biopharmaceutical logistics services.

Stringent Regulatory Requirements

Compliance with Good Distribution Practices (GDP), Good Manufacturing Practices (GMP), and international pharmaceutical regulations is driving demand for experienced third-party logistics providers.

Market Challenges

High Cold Chain Infrastructure Costs

Developing and maintaining temperature-controlled storage facilities, transportation fleets, and monitoring systems require significant capital investment.

Regulatory Compliance Complexity

Logistics providers must comply with multiple international pharmaceutical regulations, quality standards, and product traceability requirements.

Risk of Temperature Excursions

Maintaining product integrity during transportation remains a critical challenge, particularly for highly sensitive biologic and gene therapy products.

Supply Chain Disruptions

Global transportation delays, geopolitical uncertainties, and infrastructure limitations can affect timely delivery of biopharmaceutical products.

Market Segmentation

The biopharmaceutical third-party logistics market is segmented based on service type, product type, transportation mode, end-user, and region.

By Service Type

The market includes:

- Transportation Services

- Warehousing and Storage

- Cold Chain Logistics

- Inventory Management

- Packaging and Labeling

- Value-Added Logistics Services

Cold chain logistics dominate the market due to the increasing demand for temperature-controlled transportation of biologics and specialty pharmaceuticals.

By Product Type

The market is categorized into:

- Vaccines

- Biologics

- Biosimilars

- Cell and Gene Therapies

- Blood Products

- Other Biopharmaceuticals

Biologics account for the largest market share owing to their widespread use in oncology, immunology, and chronic disease treatment.

By Transportation Mode

The market includes:

- Air Freight

- Road Freight

- Sea Freight

- Rail Freight

Air freight represents a significant market segment due to the urgent and temperature-sensitive nature of high-value biopharmaceutical shipments.

By End-User

The market is segmented into:

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Manufacturing Organizations (CMOs)

- Hospitals and Specialty Clinics

Pharmaceutical companies remain the dominant end-user segment due to increasing outsourcing of logistics operations and expanding biologics production.

Regional Insights

North America

North America dominates the biopharmaceutical third-party logistics market due to advanced healthcare infrastructure, strong pharmaceutical manufacturing capabilities, well-established cold chain networks, and the presence of leading logistics service providers. The United States remains the largest contributor to regional growth.

Europe

Europe represents a significant market supported by stringent pharmaceutical regulations, increasing biologics production, advanced logistics infrastructure, and growing demand for temperature-controlled distribution services.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth during the forecast period due to expanding pharmaceutical manufacturing, increasing biotechnology investments, growing vaccine production, and rapid development of cold chain logistics infrastructure across China, India, Japan, and South Korea.

Latin America

Latin America is experiencing steady growth driven by increasing pharmaceutical production, healthcare modernization initiatives, and improving cold chain distribution capabilities.

Middle East & Africa

The Middle East & Africa region is emerging as a promising market due to expanding healthcare infrastructure, growing pharmaceutical imports, and increasing investments in temperature-controlled logistics solutions.

Key Trends and Growth Opportunities

Digitalization of Pharmaceutical Supply Chains

Logistics providers are increasingly adopting IoT sensors, real-time shipment tracking, blockchain technology, and predictive analytics to improve visibility and product traceability.

Growth of Personalized Medicine Logistics

The expansion of personalized medicines and advanced therapies is creating demand for specialized logistics services with highly controlled transportation environments.

Increasing Investment in Smart Cold Chain Technologies

Companies are deploying automated temperature monitoring systems, connected refrigeration equipment, and AI-driven logistics platforms to improve operational efficiency.

Expansion of Biopharmaceutical Manufacturing

Growing investments in biologics, biosimilars, and vaccine manufacturing facilities are expected to create substantial long-term opportunities for third-party logistics providers.

Key Players Analysis

The biopharmaceutical third-party logistics market is highly competitive, with major logistics companies focusing on cold chain expansion, digital transformation, and specialized pharmaceutical distribution services.

Key companies operating in the market include:

- DHL Supply Chain

- Kuehne+Nagel International AG

- FedEx Corporation

- United Parcel Service, Inc.

- DB Schenker

- CEVA Logistics

- AmerisourceBergen Corporation

- Cardinal Health, Inc.

- Cencora, Inc.

- NIPPON EXPRESS HOLDINGS, INC.

These companies are investing in cold chain infrastructure, digital supply chain technologies, advanced temperature monitoring systems, and global network expansion to strengthen their positions in the global biopharmaceutical third-party logistics market.

For Detailed Insights, Visit:

https://straitsresearch.com/report/biopharmaceutical-third-party-logistics-market

About Us

Straits Research is a leading research and intelligence organization, specializing in research, analytics, and advisory services, along with providing business insights and research reports.

Contact Us

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.)